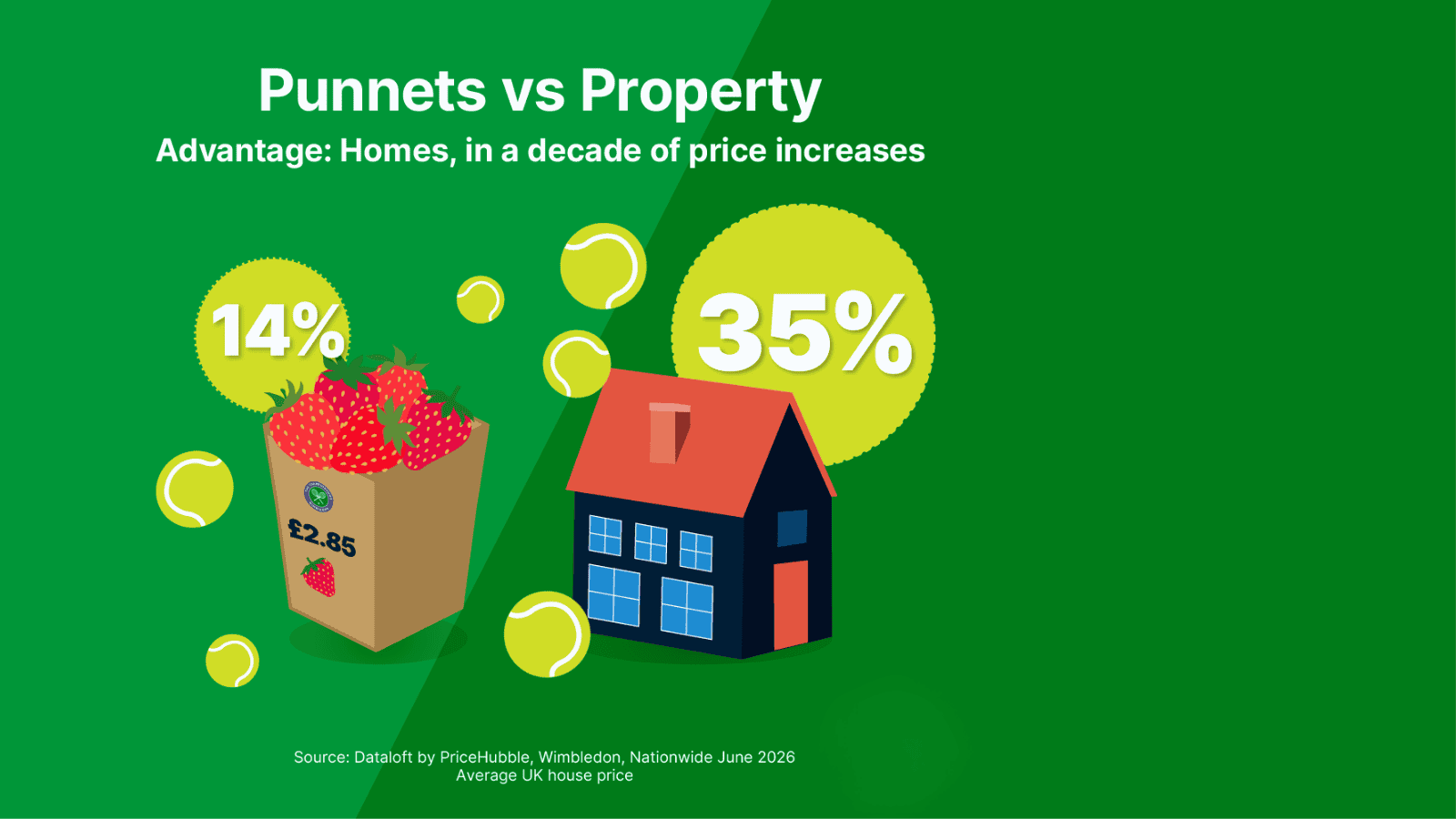

Punnets vs Property

The 139th Wimbledon Championships are underway at the All England Club, welcoming 128 singles players and 64 doubles teams in each draw ahead of the

The 139th Wimbledon Championships are underway at the All England Club, welcoming 128 singles players and 64 doubles teams in each draw ahead of the

The summer solstice, the longest day of the year and an event celebrated around the world, falls in the Northern Hemisphere on Sunday 21 June

The 2026 World Cup begins this week and stands as the largest tournament in the competition’s history, with 48 countries travelling to the United States

The UK mortgage market is demonstrating notable resilience in the face of higher borrowing costs and a more uncertain global economic backdrop. The latest data

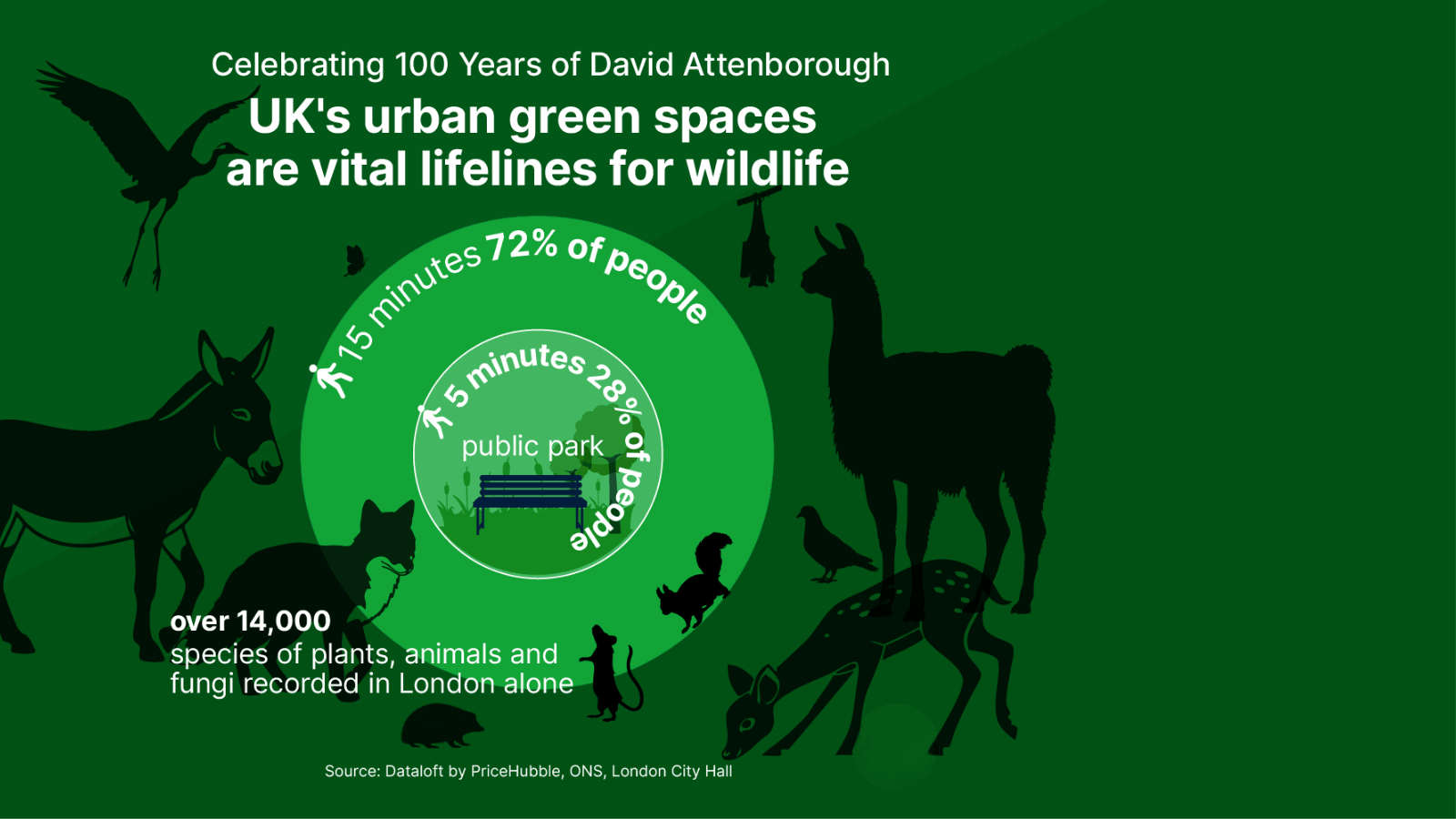

Sir David Attenborough has recently celebrated his 100th birthday, marking a remarkable century of life from a broadcaster and naturalist who has spent more than

Energy bills remain one of the most significant pressures on UK household budgets at present, and the home a person lives in has a substantial

UK annual house price growth accelerated to 2.2% in March 2026, a significant increase from the 1.0% recorded in February, indicating that the market regained

As the UK rental market approaches one of its most significant regulatory changes in decades with the Renters’ Rights Act coming into force on 1

As the new academic year draws closer, the cost of student accommodation has emerged as a decisive factor for many prospective undergraduates choosing where to

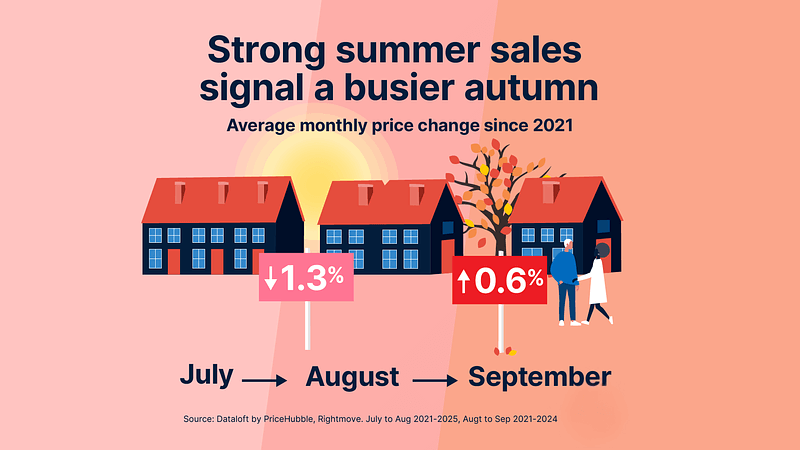

The UK housing market took its expected summer breather this August as the average asking price dipped by 1.3% to £368,740. While some may raise