Buyer Confidence Rises 2025

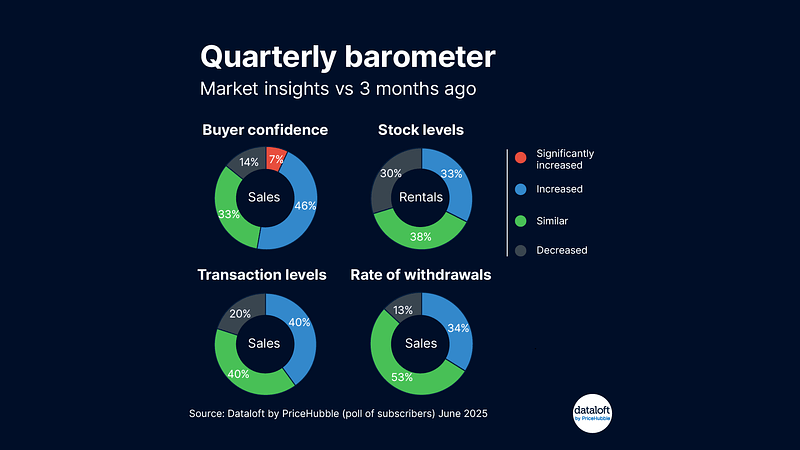

Falling mortgage rates have helped boost buyer confidence. Just over one out of two agents said conditions have improved since the last quarter. Buyer sentiment is picking up too — 46% noticed more confidence, one out of three said levels were unchanged while only 7% saw a significant jump. This shows a steady upward trend without major shifts.

Following the stamp duty lull, transaction volumes bounced back strongly between April and May, rising by 25%. Still, only 40% of agents felt transaction levels matched the previous quarter. Meanwhile, 20% reported a decline, pointing to a recovery that’s still uneven.

Sales withdrawals remain stable. Around one out of two agents said the rate hasn’t changed while 34% noticed a decrease and 13% saw an increase. This suggests most sellers are staying the course.

In the rental sector, demand is steady but supply is tight. 38% of agents reported a drop in available rental properties, one out of three said levels have stayed the same while 30% saw an increase. This reflects growing pressure on rental stock.

Overall, the data suggests a market regaining momentum, led by improving buyer confidence and rising transactions though supply challenges and regional differences remain.

Buyer Confidence Rises 2025 Read More »