Beyond the Averages: What London’s Rental Market Really Tells Us

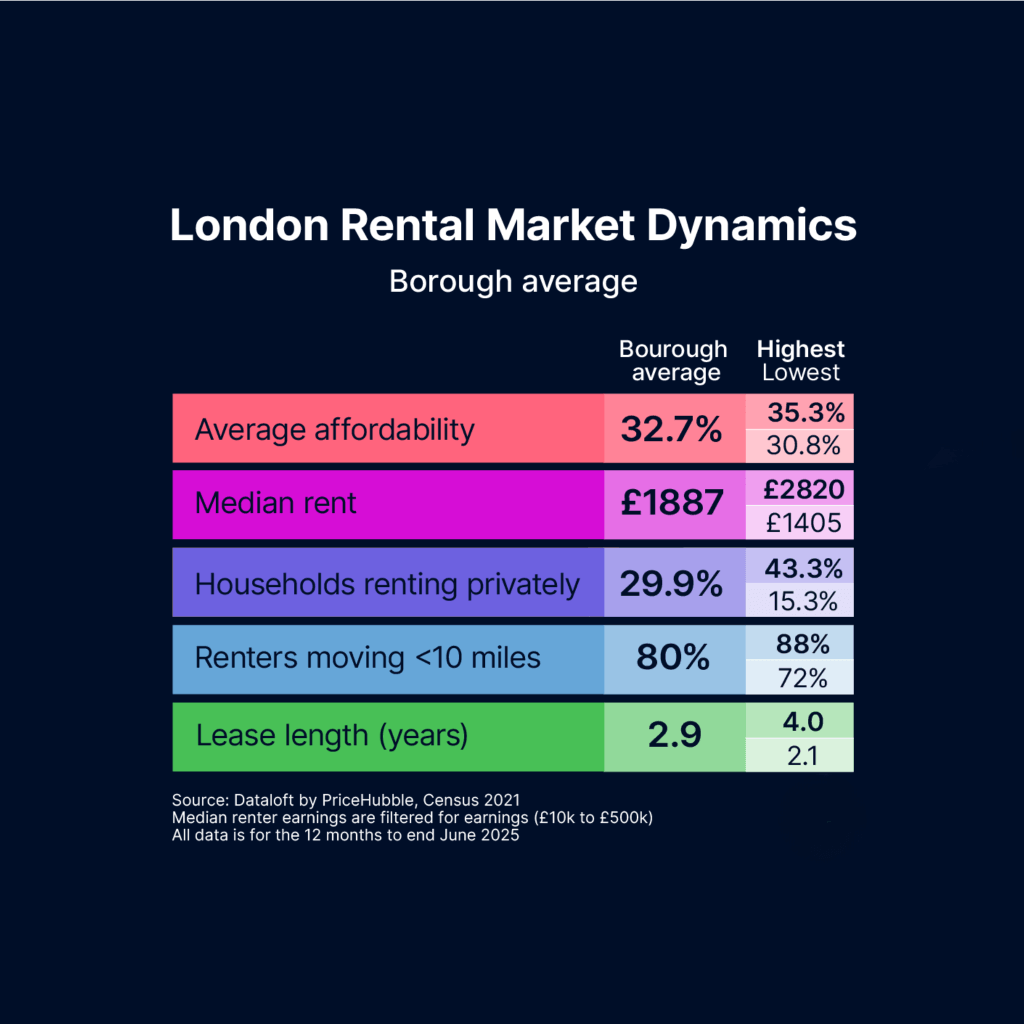

Headline averages are useful but they only scratch the surface. To truly understand the dynamics of London’s rental market it is essential to look borough by borough. While certain themes run consistently across the capital the data also reveals striking local contrasts.

Across all London boroughs renters are devoting more than 30% of their income to rent. Havering sits at the lowest end of the spectrum at 30.1% while Hammersmith & Fulham tops the chart at 35.3%. This underlines the universal pressure that rent places on household budgets regardless of location.

The average rent in London now stands at £1,887 per calendar month. Yet the borough breakdown shows wide disparities. Kensington & Chelsea commands the highest rents at £2,820 pcm while Bexley offers the most affordable average at £1,405 pcm. For tenants this gap highlights just how dramatically housing costs can shift depending on postcode.

Another area of divergence lies in the proportion of households relying on the private rental sector. Bexley has the smallest share at 15% whereas Westminster sees almost half its households—43%—renting privately. Such figures demonstrate how ingrained private renting has become in some parts of London compared with others where homeownership still holds greater sway.

London’s rental market is also highly localised. On average 80% of new lets are taken by renters moving within a 10-mile radius. This reflects not only lifestyle preferences but also the strong pull of community ties, workplaces or local amenities. The average lease length across London is 2.9 years but this masks variation. Some boroughs see tenants staying for just 2.1 years while in others leases stretch to 4 years. These patterns reveal different levels of stability or transience in local rental markets.

The capital’s averages provide a useful headline but the borough-level data paints a much richer picture. From affordability pressures to the dominance of renting in certain areas London’s rental market is shaped by local realities as much as citywide trends.

Beyond the Averages: What London’s Rental Market Really Tells Us Read More »