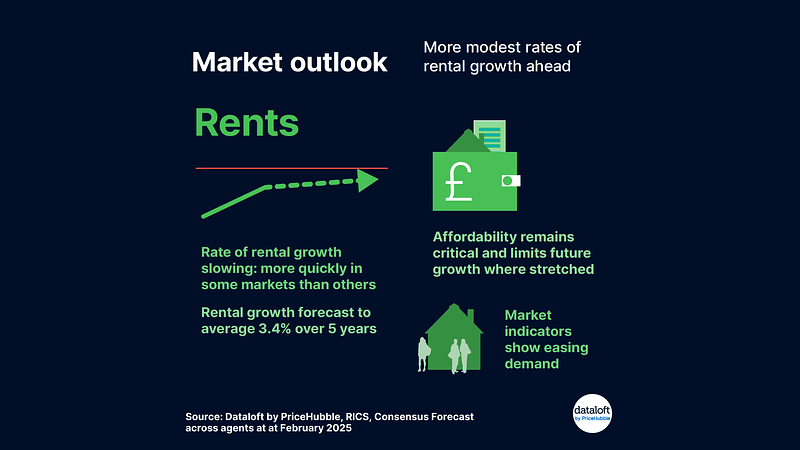

Market outlook: More modest rates of rental growth ahead

After years of high rental growth, the pace of increases in achieved rents for new market lets is slowing, with some markets experiencing this deceleration more rapidly than others.

A key factor influencing this trend is affordability, which constrains further growth where financial strain is evident. In London, for example, affordability has reached just above 32%, contributing to a significant slowdown in rental growth from 9.0% a year ago to 1.7% currently.

Additional market indicators, such as data from RICS, suggest a normalisation in both demand and supply levels, particularly for demand, which had been elevated in recent years. As a result, rental growth is expected to stabilise, with an average annual increase of 3.4% projected over the next five years.

With reduced pressure in the market, rental turnover may rise, as previous tight conditions led many renters to renew existing leases rather than move. This shift towards more modest growth reflects a broader market adjustment in response to affordability constraints and easing demand.

Market outlook: More modest rates of rental growth ahead Read More »