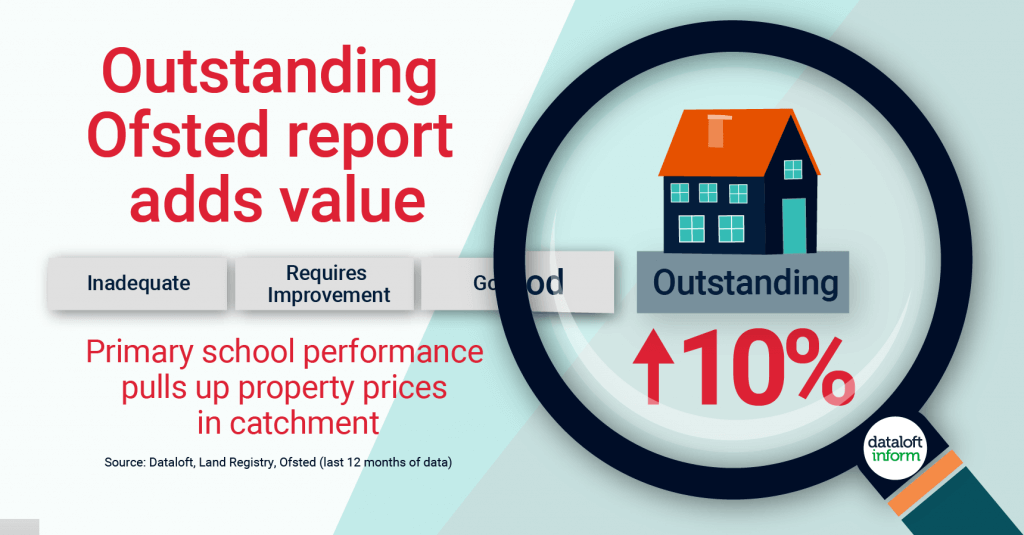

Does a good Ofsted report affect property prices?

- House prices are significantly higher in the catchments of Ofsted ‘outstanding’ primary schools, even compared to those ranked ‘Good’ in their Ofsted report.

- Average sale prices are 10% higher around a primary school with outstanding status, (based on £ per sq ft and compared with good status), while average rents are 5% higher.

- There’s a similar price difference of 8% between ‘Good’ and ‘Requires improvement’ – the next Ofsted category down. Below that, the impact on house prices seems to fall away.

- There are regional differences. The relationship between Outstanding school designations and house prices is strongest in the North West. Source: Dataloft, Land Registry, Ofsted (last 12 months

The borough of Croydon has many schools that are rated as outstanding by Ofsted. These span across the borough, incorporating Thornton Heath.

Generally, schools in the South Croydon area help properties to command a higher asking price than properties in Thornton Heath, as well as, East and West Croydon. This is despite the latter locations offering superior transport links and a shopping centre.

If you are thinking of moving in or out of the Croydon Borough and would like to get an idea of property prices, please give us a call on 0330 043 0002 and speak with one of our friendly Property Experts who will be happy to assist you.

Leigh Thomas – Truuli Property Expert

Does a good Ofsted report affect property prices? Read More »